Climate Change and Bank Deposits: How Abnormally Warm Temperatures Trigger Depositor Discipline of Fossil-Fuel-Financing Banks

Initiative in Sustainable Finance: Research Highlight by Prof. Steven Ongena and Co-Author

The paper studies whether households discipline banks that finance fossil fuels by reallocating their deposits when they personally experience unusually warm weather, a salient manifestation of climate change.

Authors:

- Özlem Dursun-de Neef, Monash Business School

- Steven Ongena, University of Zurich, Swiss Finance Institute

“When people experience unusual heat, climate change becomes more salient, and deposit growth at fossil fuel financing banks weakens.”

- Dr. Özlem Dursun de Neef

Introduction

The study combines local temperature anomalies, NGO campaigns that publicly name “brown” banks, and detailed U.S. branch-level deposit data to trace how climate-related beliefs translate into financial behavior. Central is the interaction between abnormal temperatures, political/climate beliefs (Republican vs. non-Republican counties), and banks’ fossil fuel exposures.

Methodology

The authors merge U.S. county-level temperature data from NOAA (1900–2021) with FDIC branch-level deposits, deposit rates (RateWatch), fossil-fuel financing from the “Banking on Climate Chaos” report (top 60 global lenders), Yale Climate Opinion Maps, and 2016 U.S. county election results.

Abnormal temperatures are defined as deviations from 100-year historical monthly averages, aggregated into 12-month moving averages of positive anomalies to capture warmer than usual conditions at county level.

They estimate panel regressions of deposit growth on abnormal temperatures interacted with a fossil fuel bank dummy, using bank×year and county×year fixed effects to compare the same bank across counties and to absorb local shocks. Additional regressions relate abnormal temperatures to climate belief measures, exploit cross-sectional heterogeneity by Republican vote share, and use an IV strategy that instruments beliefs with abnormal temperatures in the post-2016 period when NGO disclosure starts.

Robustness checks vary temperature windows, use cold anomalies, alternative historical baselines, exclude COVID19 years, and control for bank heterogeneity (CAMELS-type characteristics).

“We find significant deposit reductions for fossil-fuel-financing banks relative to other banks in counties with higher abnormal temperatures. Specifically, a 1°F increase in the abnormal temperature is associated with a 1.6 percentage point (pp) relative reduction in the deposit growth rate of fossil-fuel-financing banks.”

- Prof. Steven Ongena

Figure 3. Total fossil fuel financing during 2016–2021

This figure presents the total fossil fuel financing provided by the top 60 banks during our sample period of 2010–2021. The data is collected from the “Banking on Climate Chaos” report.

Key Findings

- A 1°F increase in annual abnormal temperature leads to about a 1.6 percentage point lower deposit growth for fossil fuel financing banks relative to other banks (≈20% of mean growth; ≈USD 17 million per average bank county). In parallel, other banks gain deposits: their growth rises by about 0.8 percentage points per 1°F, indicating active reallocation rather than aggregate outflows.

-

Abnormally warm temperatures increase local climate change beliefs: a 1°F increase raises the share of residents who think global warming is happening by about 0.2%, roughly 30% of the average annual increase in beliefs. This belief update and associated deposit flight concentrate in counties with more Republican voters, i.e. where initial climate skepticism is higher; in high Republican counties a 1°F increase raises beliefs by 0.3% and significantly cuts fossil fuel bank deposit growth. In more climate aware (fewer Republican) counties, fossil fuel bank deposits are already lower, but no additional temperature-driven effect appears; deposit reductions there are independent of abnormal temperatures.

-

Fossil fuel financing banks respond by paying higher deposit rates in hotter, especially Republican, counties (more so on larger CD balances) - yet still lose deposits, pointing to prosocial rather than financial motives among depositors.

-

Larger fossil fuel exposures (“Dirty Dozen”, and categories such as fossil fuel expansion, Arctic, offshore, fracking, coal mining) produce stronger temperature driven deposit losses.

-

Cold anomalies do not move beliefs or deposits, underscoring that only heat is perceived as climate related.

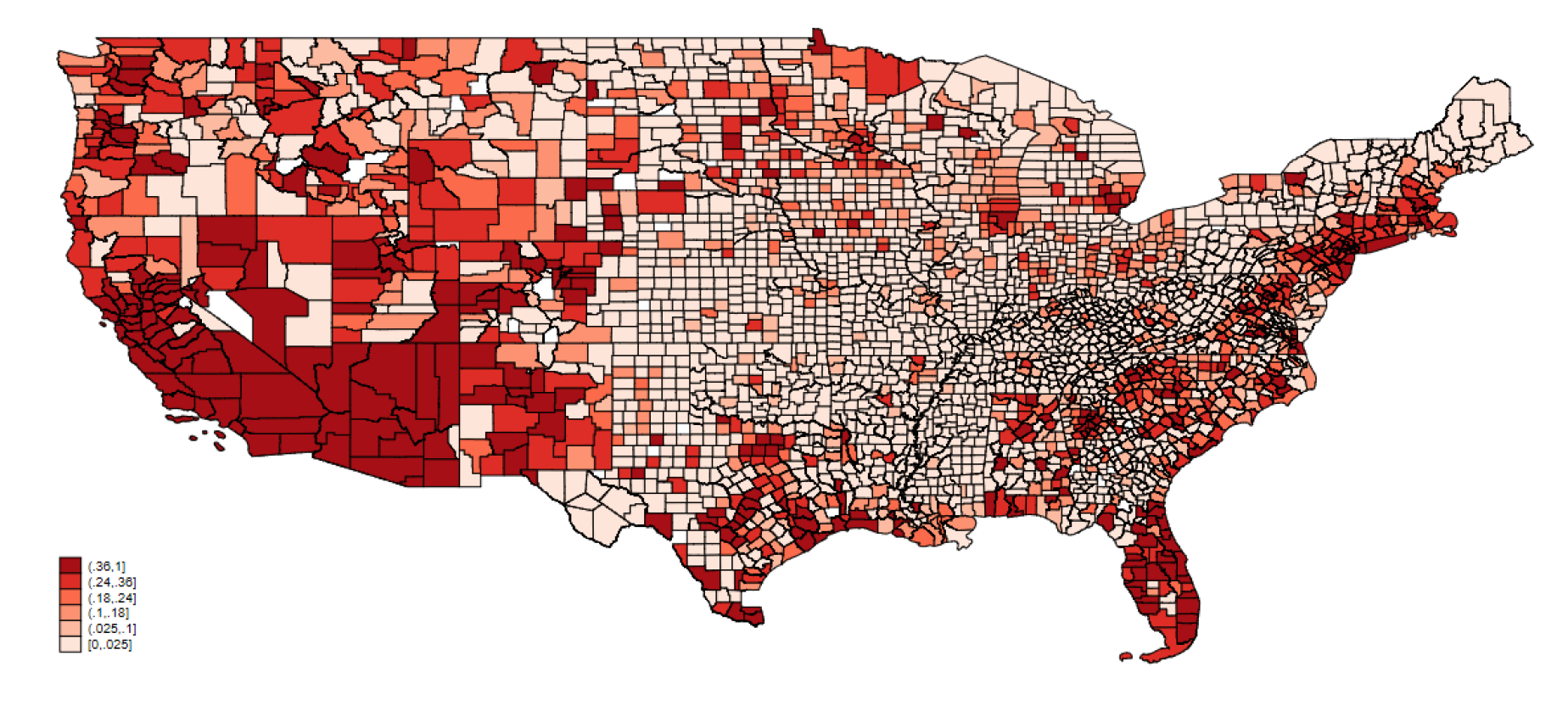

Figure 4. The presence of fossil-fuel-financing banks across counties

This figure presents the fraction of deposits in the fossil-fuel-financing banks divided by total deposits in each county, calculated in 2016.

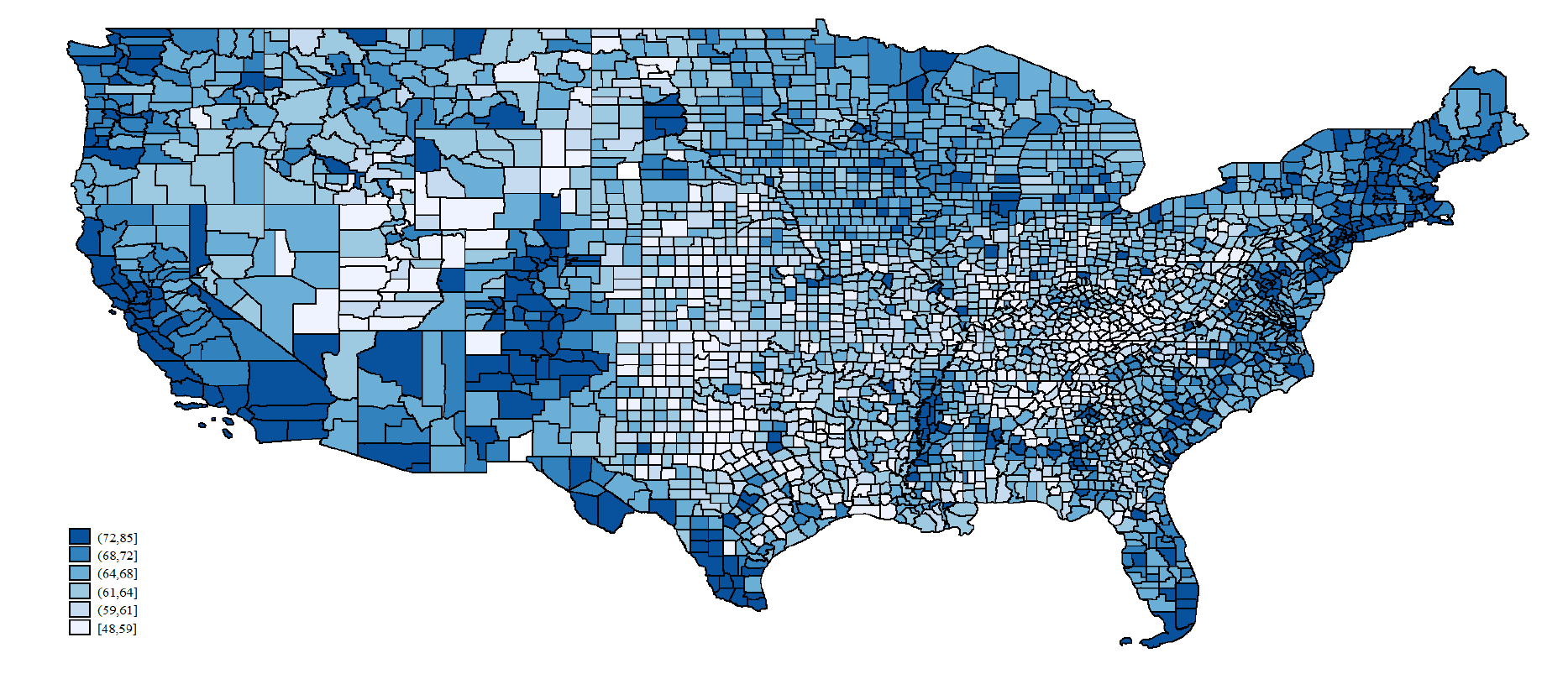

Figure 5. Climate change beliefs

This figure presents the percentage of respondents in each county that said “Yes” to the Yale Climate Survey question “Do you think that global warming is happening?” in the 2016 survey.

Implications and Conclusions

The paper shows that households can and do exert discipline on fossil fuel financing banks when climate change becomes salient through local heat shocks.

NGO disclosure (naming top fossil banks) makes these banks visible targets, while warmer than usual temperatures trigger belief updating and prosocial deposit reallocation. Banks with larger fossil exposures face greater funding risk in politically conservative areas once climate impacts are felt, despite offering return premia.

This suggests that climate-aware depositors represent a meaningful market force that can complement regulation in driving decarbonization of bank balance sheets. The results also imply that public information campaigns and climate education may amplify such bottom-up pressure on fossil fuel finance.

More Information:

Dursun-de Neef, H. Özlem and Ongena, Steven R. G., Climate Change and Bank Deposits (February 27, 2025). Swiss Finance Institute Research Paper No. 24-46, Available at SSRN: https://ssrn.com/abstract=4657847 or http://dx.doi.org/10.2139/ssrn.4657847

Photo source: Gildásio Filho via Unsplash