Economics and Biodiversity in Switzerland: Does Sustainable Investing Help to Moderate the Problem?

Initiative in Sustainable Finance: Research Highlight by Prof. Thorsten Hens and Dr. Ester Trutwin

The paper studies how the loss of biodiversity interacts with economic activity in Switzerland and whether sustainable investing can reduce environmental damage in realistic “second‑best” world with too‑low environmental prices.

The authors

- Prof. Thorsten Hens, Professor of Financial Economics and

- Dr. Ester Trutwinn Boston Consulting Group (BCG)

build on neoclassical general‑equilibrium theory, but assume that markets for environmental services (like biodiversity) either do not exist or price nature far below its true social cost. In such a setting, firms overuse biodiversity, households suffer from environmental degradation, and standard competitive equilibria are no longer Pareto‑efficient.

The key question is whether impact investing and ESG investing can partially correct this mispricing by changing how much capital households supply to firms that damage biodiversity.

Methodology

Conceptually, the authors develop a one‑period general‑equilibrium model with one representative firm and one representative household, where output is produced using capital and the environment (biodiversity) as essential inputs.

The firm maximizes profit with respect to capital and environmental use, while the household derives utility from consumption and a clean environment and supplies capital to the firm. Production is modeled with a CES production function in capital and environmental input, and household preferences follow a Cobb‑Douglas utility function in consumption and environmental quality.

The paper contrasts three regimes:

- (i) a first‑best competitive equilibrium with flexible prices for capital and environment,

- (ii) a more realistic second‑best equilibrium with an exogenously fixed, too‑low environmental price, and

- (iii) a sustainable‑investing equilibrium where households strategically withhold capital (impact investing) and where this behavior can be implemented via ESG ratings.

Empirically, the model is calibrated to Switzerland using GDP, stock‑market returns, forest‑area data, and biodiversity‑related political preferences. The elasticity of substitution and the relative productivity of biodiversity in the CES production function are estimated from Swiss consumption, stock‑market and land‑use data, while the weight households assign to biodiversity in utility is inferred from canton‑level voting on the 2024 “biodiversity initiative”.

The authors then use the calibrated model to simulate how an additional exogenous 10% loss in biodiversity affects GDP, interest rates, environmental quality, and welfare under the three regimes.

Key Findings

The theoretical model shows that when the environment is underpriced, firms pollute too much and households supply all their capital, leading to a second‑best equilibrium that is not Pareto‑efficient.

If production technology is “dirty at the margin” (more capital implies more environmental use, which holds for the CES specification used), households can increase their utility by strategically withholding part of their capital. This is defined as impact investing and implies some capital becoming stranded. With impact investing, capital supply falls, output declines, environmental use falls, and welfare rises relative to the second‑best benchmark without impact investing. The cost of capital (interest rate) can move in either direction because a scarcity effect (less capital raises returns) competes with an impact effect (cleaner environment changes marginal productivity), but in the calibrated Swiss case impact investing tends to increase the cost of capital.

In the quantitative Swiss application, welfare is highest in the ideal Walrasian equilibrium with correctly priced biodiversity, lower in the impact‑investing regime, and lowest in the second‑best regime with fixed, too‑low environmental prices.

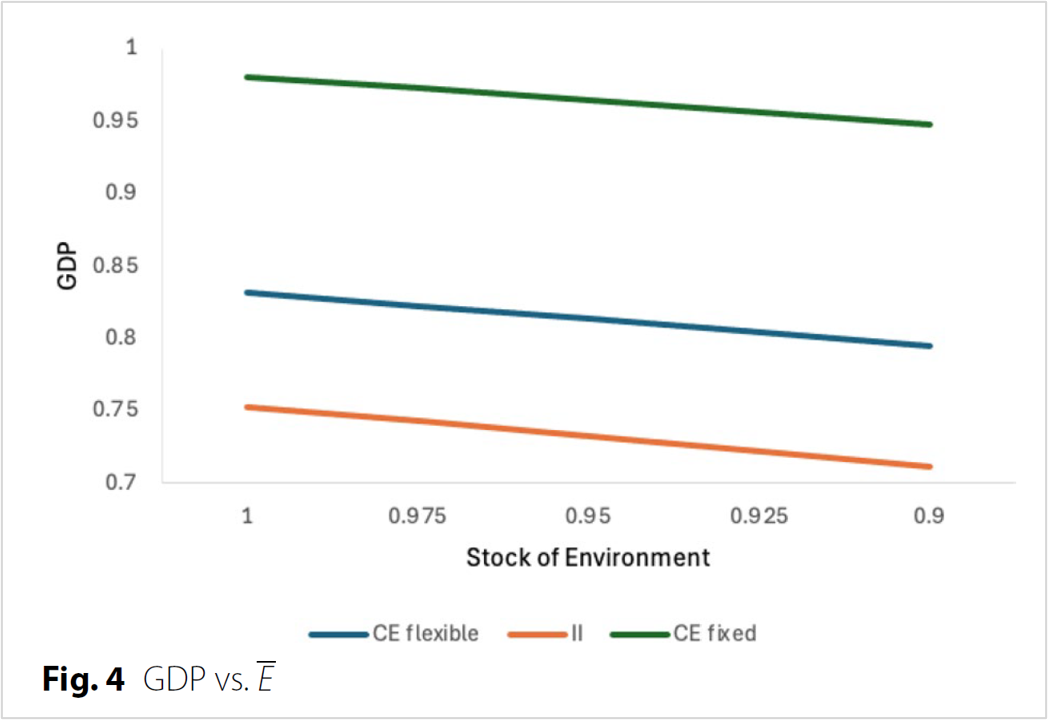

Figure 4: GDP vs. biodiversity EEE under the three regimes (competitive equilibrium with flexible prices, fixed underpriced biodiversity, and impact investing), which shows that GDP is highest with underpriced biodiversity and lowest under impact investing.

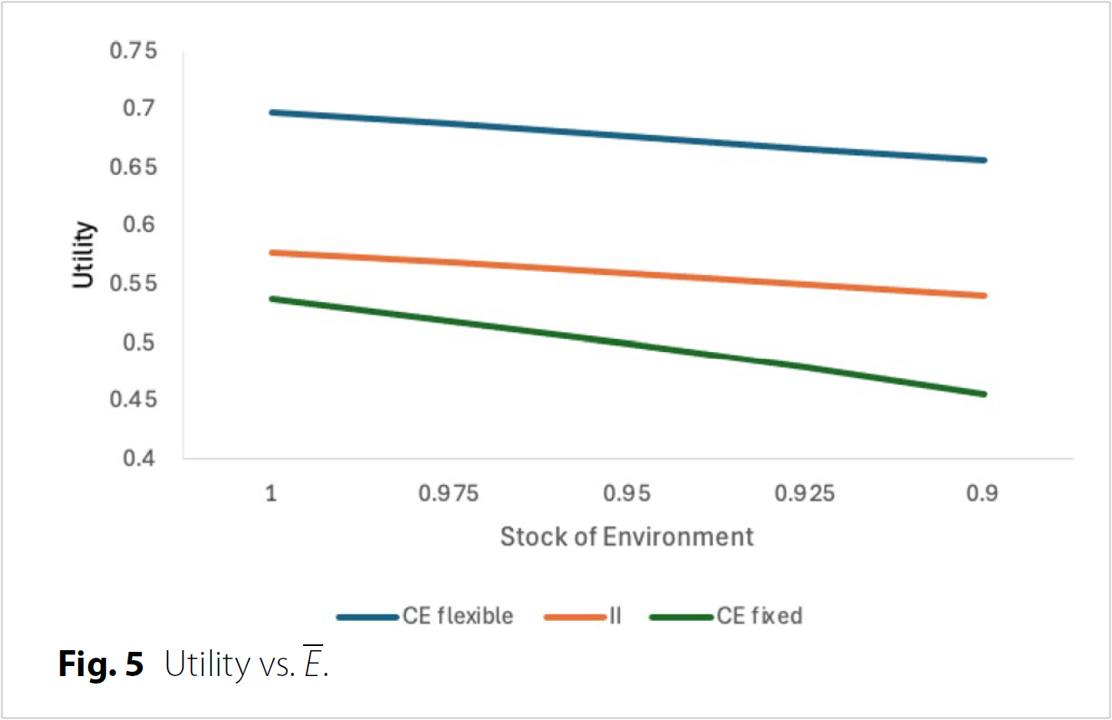

Figure 5: Welfare (utility) vs. biodiversity EEE across the same regimes, which illustrates that welfare is highest under the fully efficient equilibrium and that impact investing improves welfare relative to the second best with underpriced biodiversity.

GDP is highest under the second‑best fixed‑price regime, lower with correct pricing, and lowest when impact investing is active, reflecting the trade‑off between output and biodiversity. A further exogenous 10% loss in biodiversity leads to a GDP decline of about 4.4% under fully flexible prices, 3.4% when biodiversity is underpriced with no impact investing, and around 5.5% in the impact‑investing scenario; simultaneously, welfare and environmental quality fall most in the regime with underpriced biodiversity and no impact investing.The long‑run average Swiss equity return of roughly 8% is used as a benchmark to interpret the model‑implied changes in the cost of capital, where the simulated biodiversity loss reduces returns by roughly 0.4–0.6 percentage points depending on the regime.

Implications and Conclusions

Normatively, the paper confirms that correctly pricing environmental externalities, through fully flexible markets or Pigouvian taxes, would deliver the first‑best allocation with higher welfare and more biodiversity than any second‑best mechanism.

However, recognizing that real‑world environmental prices are politically and institutionally constrained, the authors show that sustainable investing can serve as a second‑best instrument. Impact investing, by withholding capital from environmentally harmful production, can reduce biodiversity loss and raise welfare, even though it lowers GDP and leads to stranded assets. ESG investing can, in principle, implement the same allocation as impact investing if rating agencies set ESG scores in line with firms’ marginal environmental damages and households’ marginal utility, but this requires strong information and coordination assumptions.

For Switzerland, the calibration implies that households place substantial weight on biodiversity in their preferences, consistent with (but not identical to) the canton‑level voting pattern on the 2024 biodiversity initiative. The analysis suggests that moderate biodiversity losses have economically meaningful, but not catastrophic, effects on GDP and returns, yet they significantly affect welfare and environmental quality, underscoring the importance of early action.

The authors argue that sustainable investing can “moderate” biodiversity problems but is not sufficient to fully correct the mispricing; complementary environmental policies and more dynamic, sector‑specific models are needed.

More information:

- Hens, T., & Trutwin, E. (2026). Economics and biodiversity in Switzerland: does sustainable investing help to moderate the problem? Swiss Journal of Economics and Statistics, 162, 25. https://doi.org/10.1186/s41937-026-00150-3

- Photo source: Claudio Biesele via Unsplash