Superstar Returns?

New Research Reveals Surprising Patterns in Housing Investment by Francisco Amaral

A study led by Prof. Francisco Amaral, Martin Dohmen, Sebastian Kohl, and Moritz Schularick challenges conventional wisdom about real estate investment in major cities. By assembling an unprecedented city-level dataset covering 27 cities in 15 OECD countries over 150 years, the research uncovers a striking and robust pattern: long-run total returns on residential real estate are consistently lower in large metropolitan areas than in smaller cities and rural regions.

Key Findings

- Lower Returns in Big Cities: The study finds that, on average, total housing returns in large agglomerations are about 1 percentage point (100 basis points) per year lower than in other parts of the same country. Over decades, this gap accumulates into a significant difference in wealth for homeowners and investors

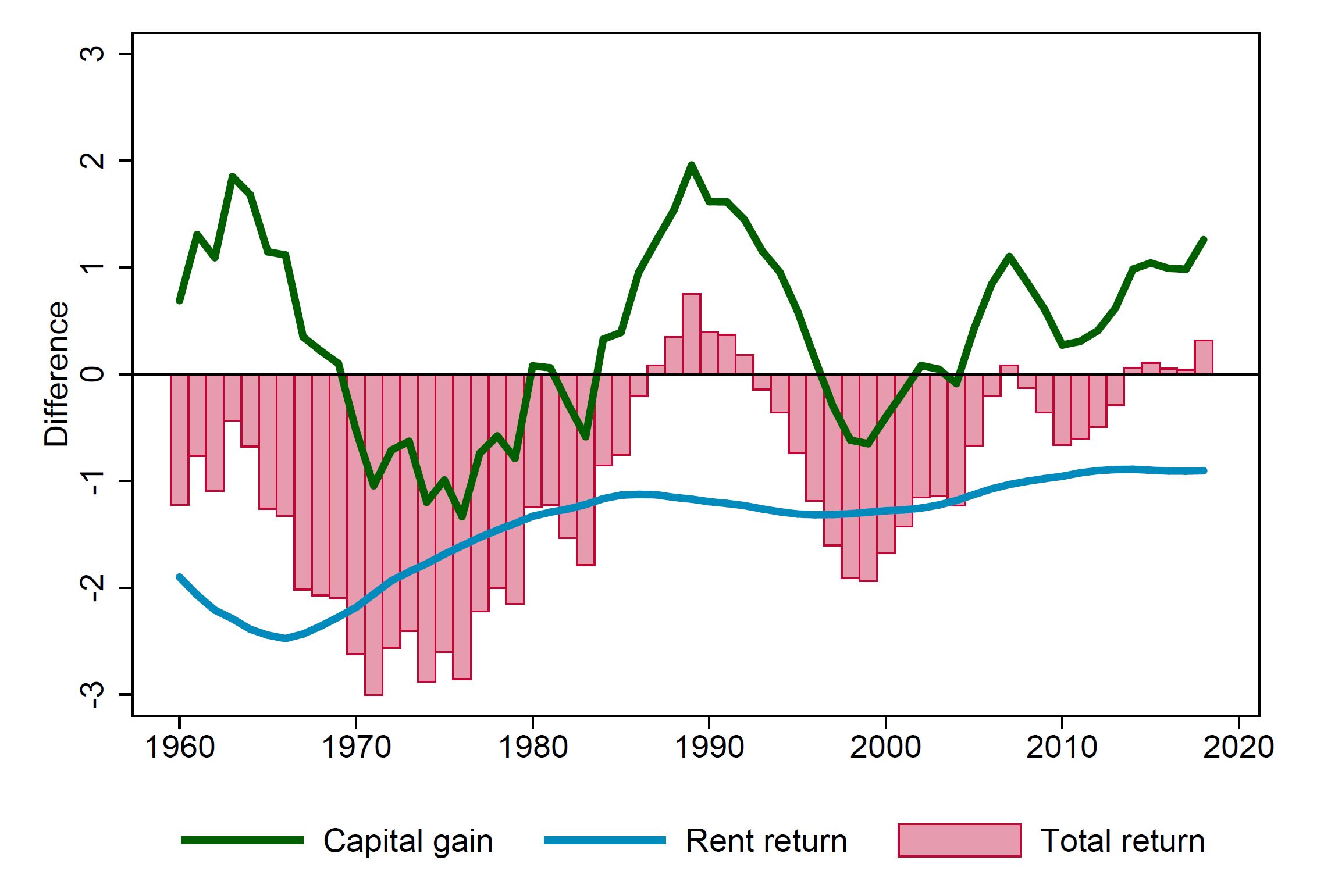

- Capital Gains vs. Rental Returns: While property values (capital gains) tend to rise faster in major cities, this is more than offset by much lower rental yields. When both capital gains and rental returns are considered, smaller cities and rural areas outperform their urban counterparts in total returns

- Risk and Liquidity Explain the Difference: The research shows that higher returns outside large cities compensate for higher risks-such as greater income volatility, higher idiosyncratic price risk, and lower market liquidity. In contrast, real estate in large, diversified cities is comparatively safer and easier to sell, allowing investors to accept lower returns

- Robust Across Countries and Eras: These patterns hold across different countries, time periods, and even after accounting for factors like rent regulation, tax regimes, and alternative definitions of metropolitan areas

Figure 10: Average differences in city-level and national returns (log points) over time, 1950-2018

Note: This graph shows 10 year lagged moving averages of the mean difference in log capital gains, log rent returns and log total returns between the city-level and the respective national housing portfolios. The return period covered is 1951 to 2018, such that the moving averages start in 1960, except for the German cities, Tokyo and Toronto, because the national data starts later for these cities.

Implications

This study fundamentally reshapes how we understand real estate as an investment. The findings suggest that the "superstar city" phenomenon-where global cities are seen as unbeatable investments-does not hold when considering total returns over the long run. Instead, the relative safety and liquidity of big-city real estate come at the cost of lower yields.

“Our results overturn the widespread belief that investing in major cities is always the best strategy. While these markets offer stability and liquidity, investors seeking higher long-term returns should not overlook smaller cities and regions. The key is understanding the balance between risk and reward in different locations.”

-Francisco Amaral

For homeowners, investors, and policymakers, these insights have far-reaching consequences. They underscore the importance of considering both risk and return, not just headline price growth, when making real estate decisions. The research also points to the need for more nuanced models in macroeconomics and urban planning, taking into account the heterogeneity within national housing markets.

In summaryThe “superstar city” is not always the superstar investment. Instead, the real estate landscape is shaped by a complex interplay of returns, risks, and market dynamics-offering both challenges and opportunities for those willing to look beyond the obvious |

More Information:

Amaral, Francisco and Dohmen, Martin and Kohl, Sebastian and Schularick, Moritz (2025). Superstar Returns? Spatial Heterogeneity in Returns to Housing, https://onlinelibrary.wiley.com/doi/10.1111/jofi.13479

Image source: Patrick Robert Doyle via Unsplash

Initiative in Sustainable Finance News